What Actually Drives Housing Returns

March 31, 2026 | Written By Christopher Collins

Conventional wisdom holds that population growth drives housing returns. The logic is intuitive — more people, more demand, rising rents.

There is truth in that view—but it is incomplete.

Over time, housing markets diverge. In some, population growth becomes pricing power. In others, it becomes new supply.

This paper introduces a framework for understanding why similar demand can lead to very different outcomes, and how a market’s ability to respond to growth shapes long-term returns.

What appears to matter most is not how much a market grows, but what that growth becomes.

Section 1 — The Population Growth Fallacy

Population growth has become one of the most widely relied-upon signals in housing. The reasoning is straightforward—more people, more demand, higher rents. It is viewed not only as a source of upside, but also viewed as a form of safety, offering downside protection. As a result, population rankings, migration statistics, and “fastest-growing city” lists have become shorthand for identifying promising housing markets.

In the short term, this logic holds. But over time, something more important happens. What appears to be structural demand often proves to be a temporary imbalance—particularly in easy-to-build markets. As new supply comes online, it absorbs the very demand that drove rents higher, and the pressure that once pushed rents upward begins to ease.

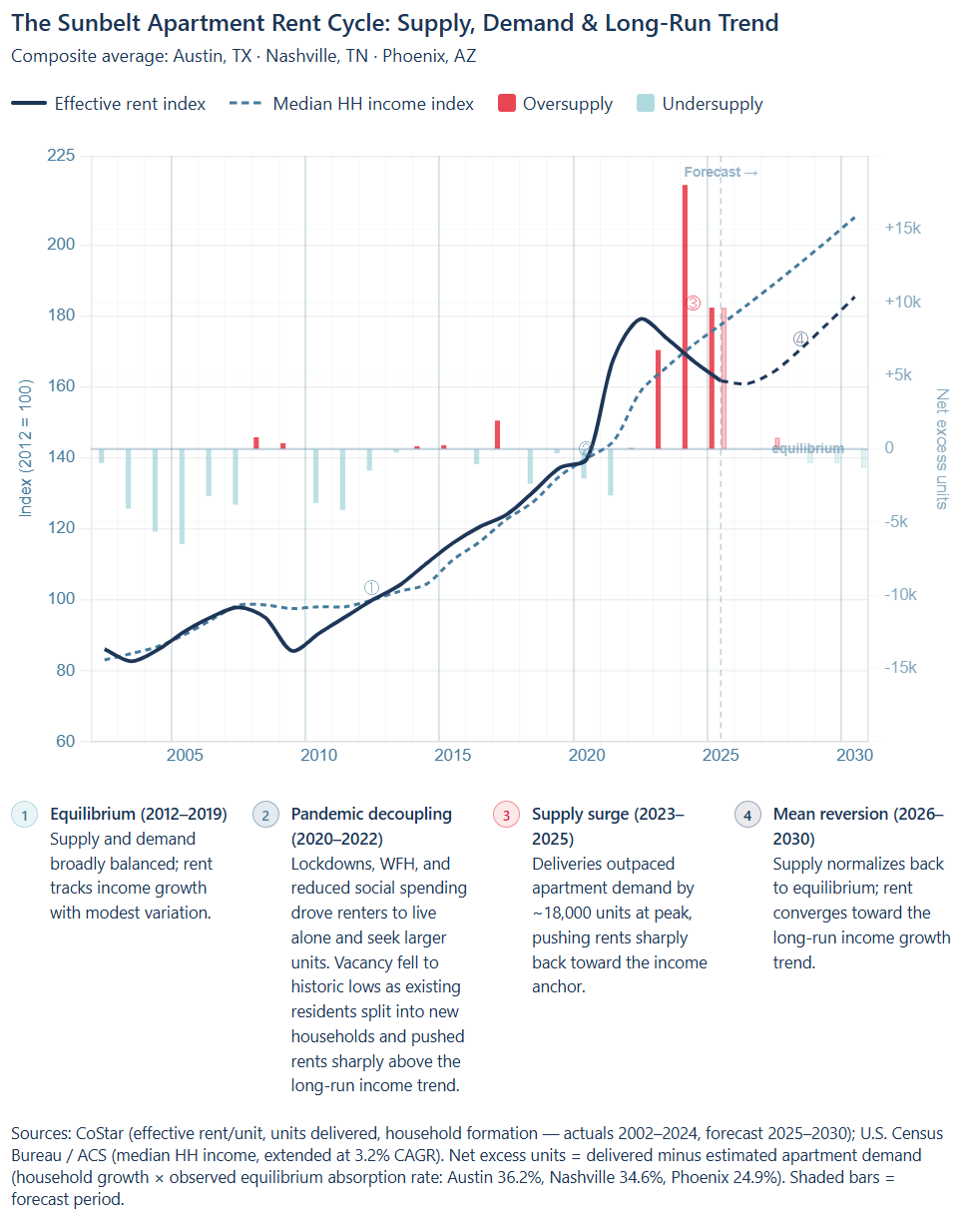

This pattern can be seen across high-growth Sunbelt markets. In cities such as Austin, Nashville, and Phoenix, COVID-era demand surged, pushing rents well above long-term income trends. But supply responded—albeit with a lag—and ultimately overshot, pulling rents back down below prior trends.

This suggests that population growth alone does not appear to drive sustained rent growth.

Section 2 — Income Growth: The Second Source of Housing Pressure

While population growth increases the number of households competing for housing, income growth increases how much those households can afford to pay. As incomes rise, households gain greater purchasing power, allowing them to compete more aggressively for available housing. Even in markets where population growth is modest, rising wages can still create meaningful upward demand pressure on rents.

Research from the Joint Center for Housing Studies of Harvard University suggests that when housing markets remain broadly balanced, rents tend to move in line with household income. This means that outside of supply constraints, rent growth generally equals income growth.

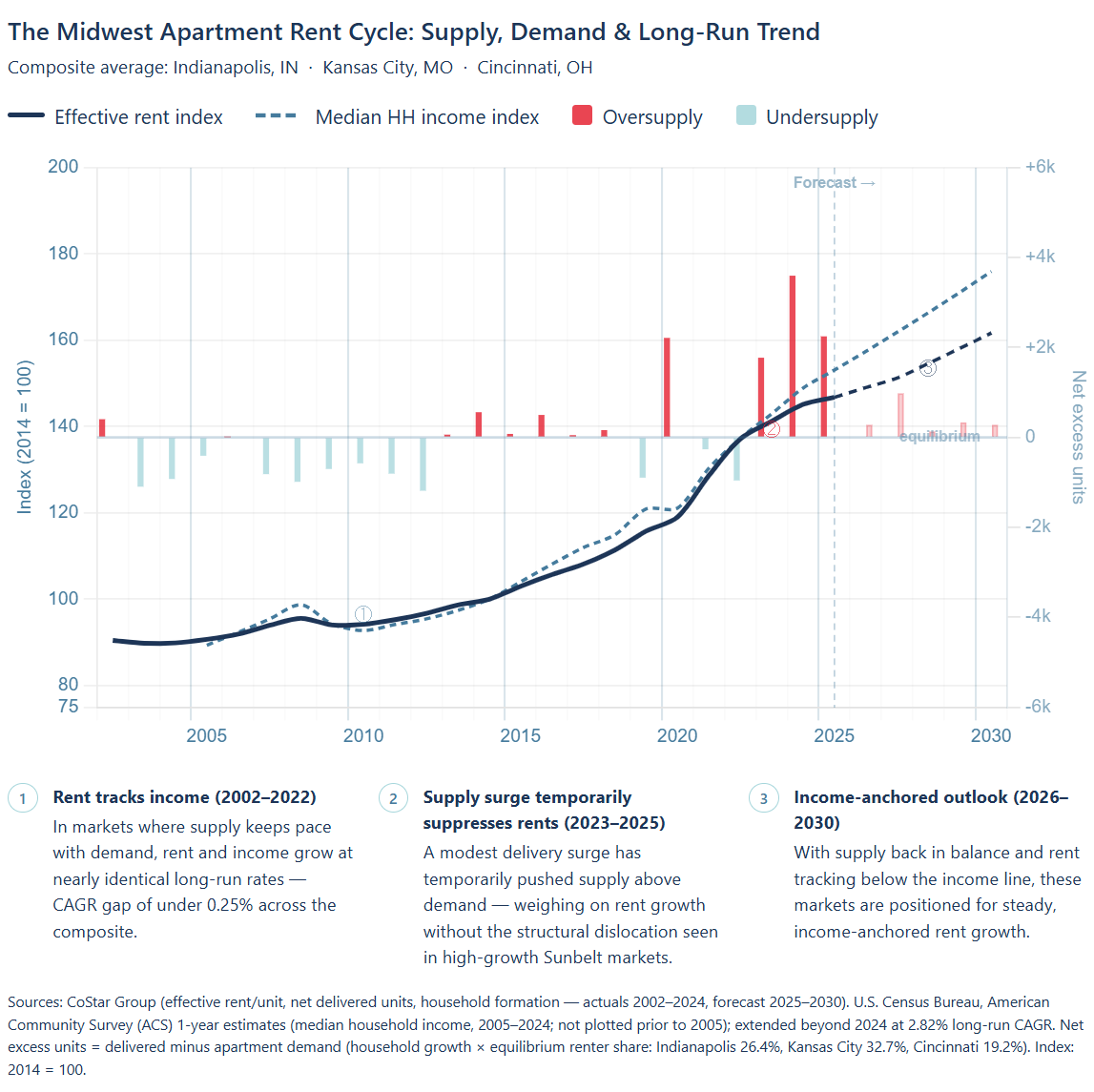

This dynamic can be observed in several Midwestern cities where population growth has remained relatively modest but income growth has steadily increased. Markets such as Indianapolis, Kansas City, and Cincinnati have experienced rising wages driven by sectors including healthcare, logistics, technology, and advanced manufacturing. Because housing supply in these markets has generally expanded alongside demand, supply and demand have remained relatively balanced. As a result, rents in many of these cities have risen steadily over time at roughly the same pace as wages. In the absence of meaningful supply constraints, rent growth has largely tracked income growth.

Section 3 — Supply Elasticity: The Housing Pressure-Valve Model

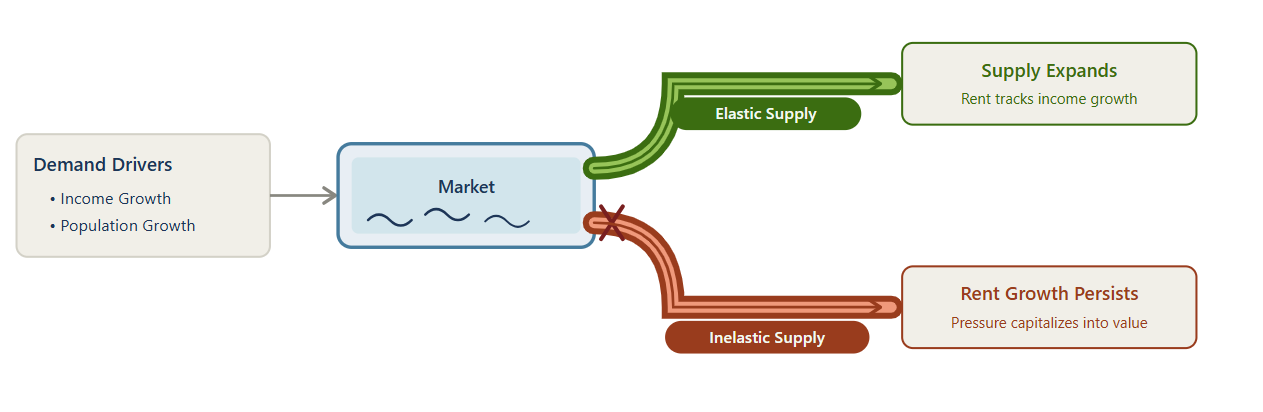

While population growth and income growth both increase housing demand, neither determines rent growth on its own. The critical variable shaping housing outcomes is how easily new housing supply can respond to that demand.

Research by housing economists such as Edward Glaeser (Harvard University), Joseph Gyourko (University of Pennsylvania’s Wharton School), and Albert Saiz (MIT) shows that when housing demand increases, markets with flexible supply tend to respond with new construction, while markets with constrained supply tend to respond with higher housing costs instead.

In practical terms, this dynamic can be thought of as a housing pressure-valve model.

When population growth or rising incomes increase demand for housing, pressure begins to build within the market. More households—and households with greater purchasing power—begin competing for the same housing stock, pushing rents upward.

In markets where development is relatively easy—typically due to abundant land, permissive zoning, and streamlined development processes—the pressure valve opens and demand is pressure released through new construction.

In markets where supply is constrained, however, that demand pressure cannot be released through development. Instead, it becomes embedded in the existing housing stock, allowing rents and housing values to rise more persistently over time.

Supply constraints monetize demand.

Section 4 — Understanding the Sources of Supply Constraints

Supply constraints can emerge from several different forces. Broadly speaking, housing markets tend to experience three primary forms of constraint: geographic limitations, regulatory barriers, and political or social resistance to development. Each of these forces can slow the ability of housing supply to respond to demand, but when multiple constraints overlap, the effects can become far more powerful.

A. Geographic Constraints

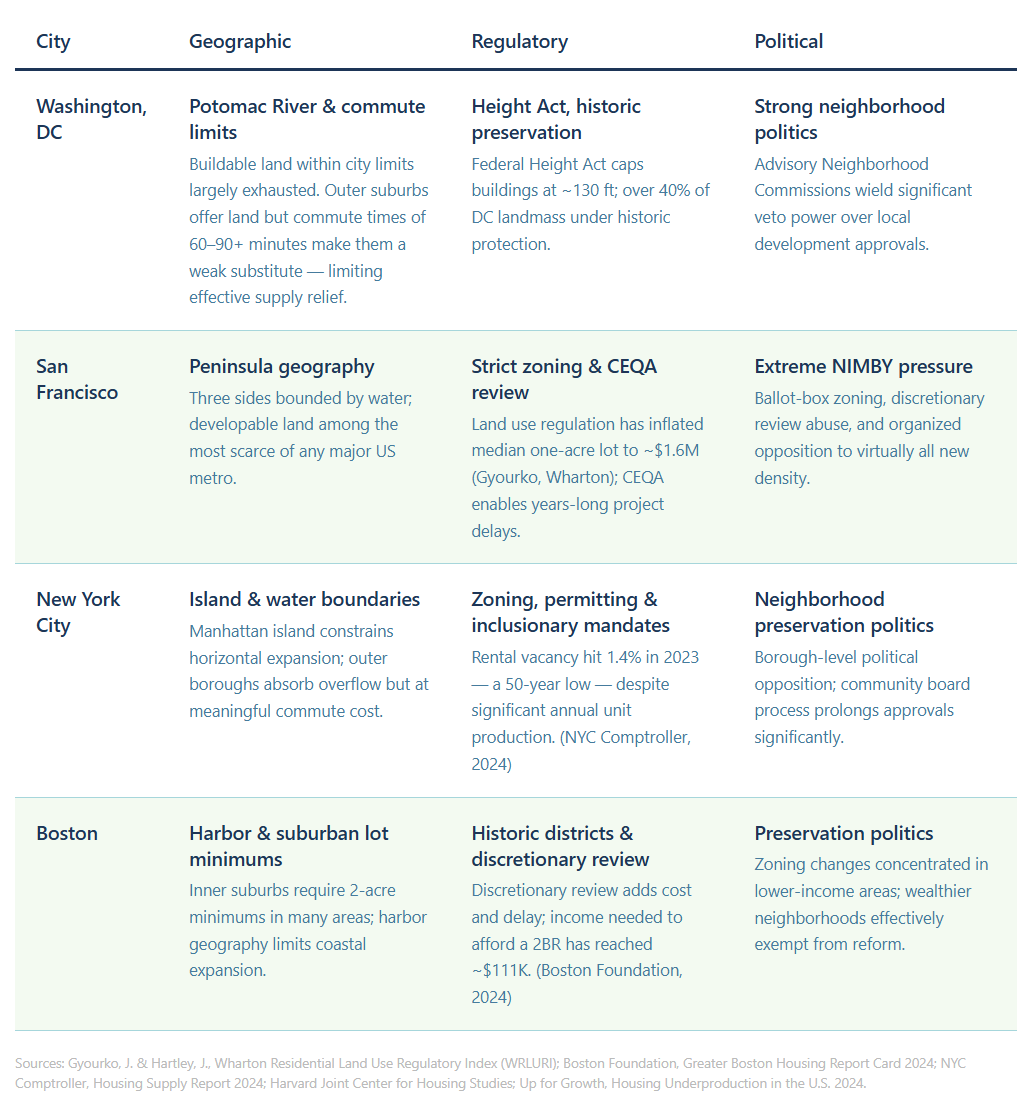

Some cities face geographic constraints where natural barriers limit the ability of housing supply to expand outward. Water, mountains, protected land, and other physical features can significantly reduce the amount of developable land available for housing.

Cities such as Miami and Honolulu illustrate this dynamic clearly. Miami is bounded by the Atlantic Ocean to the east and the Everglades to the west, leaving little room for outward expansion. Honolulu, located on the island of Oahu, faces an even more extreme constraint, with the Pacific Ocean on one side and steep mountain ranges limiting development on the other.

In markets where land availability is physically limited, housing supply often shifts from horizontal expansion to vertical development. Rather than growing outward through suburban sprawl, cities respond through higher-density construction—taller buildings and more intensive land use.

Even so, geographic constraints alone do not necessarily prevent supply from responding to demand. If regulatory and political conditions allow density to increase, housing supply can still expand through vertical development.

B. Regulatory Constraints

Other markets face regulatory constraints, where development is limited not by land availability but by rules governing what can be built and how quickly it can be approved.

Zoning restrictions, density limits, environmental reviews, permitting timelines, and complex entitlement processes can all significantly slow the pace of new housing construction.

Los Angeles illustrates how housing costs can be driven more by regulation than geography. Despite sitting on the Pacific Ocean, the City of Los Angeles spans roughly 470 square miles, and the broader region stretches outward through extensive suburban sprawl. The scale of this expansion demonstrates that land availability is not the primary constraint. Instead, zoning restrictions, density limits, environmental reviews, and lengthy entitlement processes often prevent housing supply from responding quickly to demand.

A similar dynamic exists across much of Silicon Valley, including cities such as San Jose, where housing supply remains constrained despite strong demand and relatively ample land. In these markets, development capacity is often limited by zoning restrictions, approval timelines, and other regulatory barriers rather than physical limitations.

Unlike geographically constrained cities where land is physically limited, regulatory constraints are the result of policy choices that shape how housing markets function.

C. Political and Social Constraints

In some markets, housing supply is constrained primarily through political or social resistance to development, even when land and regulatory frameworks might otherwise allow new construction.

Neighborhood opposition to density, historic preservation protections, and concerns about infrastructure capacity can all create significant barriers to housing expansion.

Charleston, South Carolina illustrates this dynamic particularly well. Much of the historic peninsula is subject to strict preservation rules and architectural review, with height limits and design regulations intended to protect the city’s historic character. While these policies preserve Charleston’s architectural heritage, they also limit the pace and scale of new housing development in the city’s historic core.

Similar dynamics can emerge in smaller metropolitan areas where rapid growth begins to strain local infrastructure. Concerns around traffic congestion, school capacity, or utilities can lead communities to resist higher-density development even when housing demand is strong. Rock Hill, South Carolina—one of the fastest-growing cities in the country—recently implemented a development moratorium due to local political pressure and infrastructure concerns.

In these cases, housing supply becomes constrained less by physical land limits and more by local political dynamics and community preferences around growth.

The Constraint “Trifecta”

In some cities, these constraints do not exist in isolation but instead overlap and reinforce one another.

Cities such as Washington, D.C., New York, San Francisco, and Boston exhibit what might be described as a housing constraint “trifecta” — geographic limitations, regulatory barriers, and strong political resistance to new development.

In these markets, developable land is limited, development approvals are complex, and local politics often slow efforts to expand housing supply.

As a result, when housing demand increases, these markets are far less able to respond with new construction. The pressure cannot be released through development.

In these environments, housing begins to behave less like a commodity and more like a scarce asset.

Importantly, supply constraints alone do not guarantee strong housing performance. Constraints can only monetize demand if demand also exists.

The markets that have historically produced the most durable housing returns tend to combine both forces —supply constraints “trifecta” and powerful economic engines.

Section 5 — Economic Engines

Population growth and income growth both increase housing demand, but when viewed over longer time horizons, both are ultimately reflections of the city’s economic engines.

Cities anchored by powerful economic engines — such as government, technology, finance, research, or healthcare — tend to generate sustained job creation and rising incomes over time. So when these strong economic engine cities operate within supply constrained housing markets, the result can be a powerful compounding dynamic.

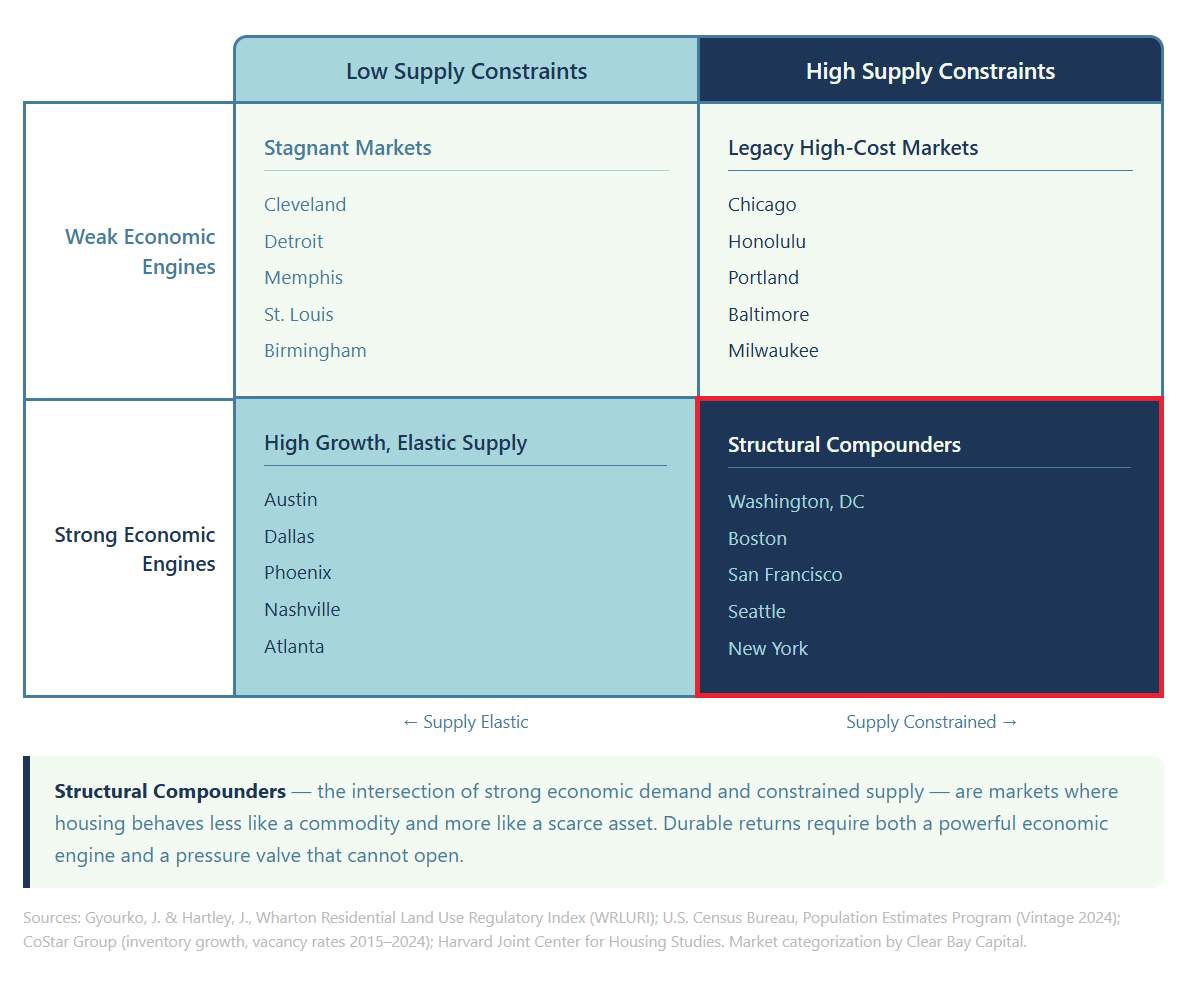

This relationship is illustrated through a simple framework comparing economic engines with housing supply constraints.

Stagnant Markets: Weak Engines, Flexible Supply

Markets with weaker economic engines and relatively flexible housing supply tend to behave most like commodities. As discussed earlier, when supply can respond easily to demand, long-term pricing power is limited.

Cities such as Cleveland, Detroit, Memphis, and St. Louis broadly fit this category. Population and income growth have generally been modest, while land availability and development constraints are limited.

As a result, these markets often offer attractive current yields, but typically produce more modest rent growth and appreciation over long periods of time.

Legacy High-Cost Markets: Constrained but Slow-Growing

Some markets exhibit meaningful supply constraints but lack strong economic growth.

Cities such as Chicago, Honolulu, Baltimore, and Portland illustrate this dynamic. Development can be constrained by zoning, preservation policies, or geographic limitations, keeping housing costs relatively elevated.

However, without strong demand engines, supply constraints alone tend to maintain price levels rather than drive sustained rent growth.

High Growth, Elastic Supply

Many of the fastest-growing metropolitan areas combine strong economic growth with relatively flexible housing supply.

Cities such as Austin, Dallas, Phoenix, Nashville, and Atlanta exemplify this dynamic. As discussed earlier, while demand has grown rapidly, housing supply has expanded just as quickly, often producing strong growth followed by waves of new construction that moderate rents.

Structural Compounders: Strong Economic Engines and Constrained Supply

The most durable housing markets combine powerful economic engines with meaningful limits on housing supply. Cities such as Washington, D.C., Boston, San Francisco, Seattle, and New York exemplify this dynamic. Their economies generate sustained demand, while geographic, regulatory, and political barriers limit the ability of housing supply to expand.

These cities have become among the most expensive places in country to live, and people keep coming anyway. That persistent willingness to pay a premium — sustained across decades and economic cycles — is what compounding looks like in practice.

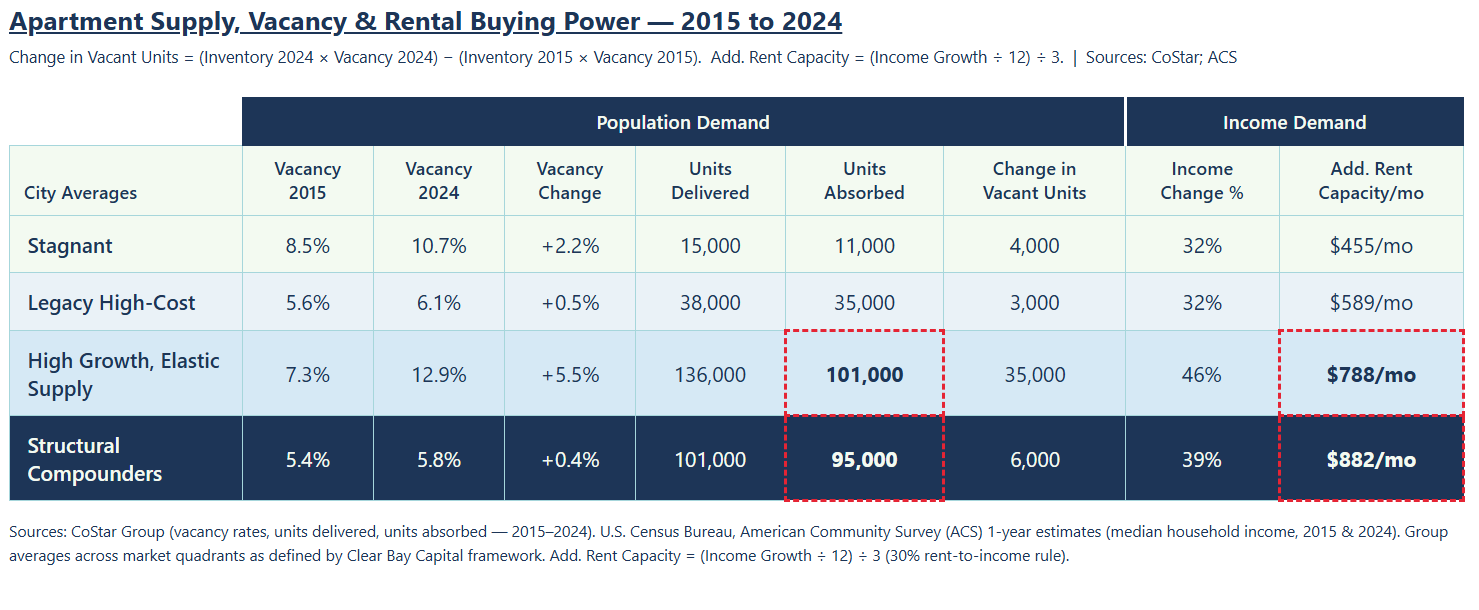

The data in the chart below from 2015 to 2024 reinforces this. On the demand side, structural compounders absorbed nearly as many units as high-growth markets—95,000 versus 101,000—indicating similar demand on an absolute basis. And on the income side, they generated more incremental rental buying power than any other category, with median household income being able to afford an additional $882 per month in rent over that same time period.

These are deep, durable markets where demand pressure has nowhere to go but into rents and values and a renter base who can pay it.

Section 6 — Washington D.C.

In our view, Washington, D.C. is a market where the conditions for long-term compounding are well aligned, yet maybe not fully appreciated.

D.C.’s demand base is not just large (7th largest MSA)—it is resilient and increasingly dynamic. The region combines one of the most educated populations in the country (63%+ bachelor’s vs. ~35% nationally) with a high-income renter base (~$100k median household income vs. ~$75k nationally). Its economy has also diversified, non-government employment now reaches ~80% of the employment base and growing, reflecting the growing private-sector activity across policy, defense tech, and AI. D.C. sits at the center of what we view as the “thinking economy”—where decisions are made, standards set, and capital allocated. While innovation may be distributed, governance, regulation, and national security remain geographically tethered—and concentrate here.

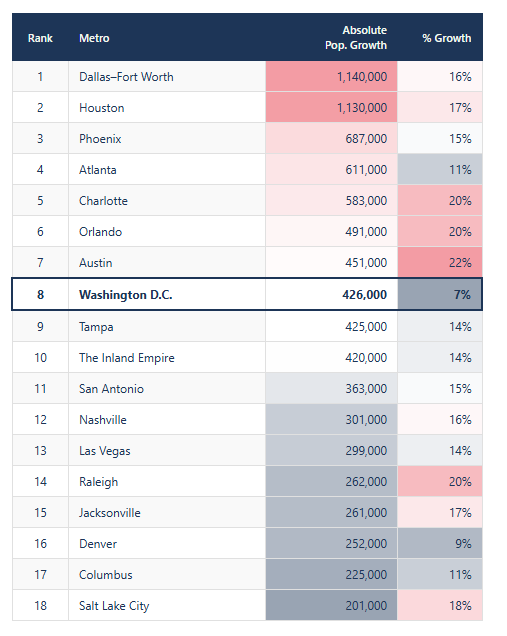

Despite persistent “coastal exodus” narratives, D.C. continues to grow. As shown in the chart, since 2015, D.C.has added more people than Nashville, Las Vegas, Raleigh, Jacksonville, and Tampa—markets often viewed as higher growth.

Supply constraints are both structural and practical. Height limits, zoning, historic preservation, and geography restrict new supply where demand is strongest, while commute realities limit outward expansion.

Whether current pricing fully reflects this dynamic is a question of market cycles and entry points — a topic we'll explore separately. What matters here is the structural picture: In this environment, incremental demand is more likely to be capitalized into rents and values than absorbed through new construction. Durable demand, constrained supply, and a deep base of human capital together create a dynamic that is difficult to replicate.

Section 7 - Framework Limitations

Every framework has its limits, and it is worth being explicit about them.

First, the cities referenced throughout this paper are illustrative, not fixed categorizations. Markets evolve. A city with relatively elastic supply today may face tighter regulatory or political constraints over time, just as a historically constrained market may loosen at the margin. The objective is not to label markets, but to highlight a structural relationship: when supply cannot respond to demand, that demand is capitalized into asset values. Which markets exhibit that dynamic at any point in time is a separate—and ongoing—judgment.

Second, this framework does not attempt to predict how secular demand drivers will unfold. Remote work, AI-driven labor shifts, and demographic changes are all meaningful, but inherently uncertain. What can be said with more confidence is that supply constraints tend to be structural, while demand is more variable. The interaction between the two differs across markets, asset types, and time horizons—and will continue to. Understanding how demand evolves matters, but it is distinct from the mechanism described here.

Finally, this is not a view on short-term pricing or timing. Supply constraints shape long-term outcomes; they do not determine near-term movements in rents or values. Cycles, interest rates, and shocks will continue to drive volatility. Those are questions of timing and entry point—and they require a different lens.

What this framework does suggest is narrower, but more durable: over long periods, where demand consistently meets constrained supply, housing has tended to compound—with persistence. That outcome is not coincidental. It is structural.

Key Takeaways:

Over the past decade, real estate narratives have centered on population growth. That focus is understandable — growth is visible and measurable. But demand alone doesn't determine housing outcomes. What matters is whether supply can meet that demand.

For investors with long-term horizons, this distinction carries particular weight. Supply-constrained markets don't always produce the fastest early returns — but they tend to produce something more valuable: persistent, structural rent growth that compounds quietly over time. That is precisely the profile that rewards patient capital.

The question isn't whether supply constraints matter — the evidence is clear that they do. The more interesting question is whether the market is pricing them correctly. Right now, we think it isn't. Capital has followed growth narratives. That leaves constrained compounders — cities where supply cannot meet demand — relatively underappreciated, and that may be an opportunity.